Why Buy Now Pay Later Apps Could Destroy Your Holiday Shopping Budget

The holiday season can be merry, cheery, and downright expensive. From holiday meals to gifts to travel, no time of the year is more likely to strain your budget than the holidays are. Under normal circumstances, this would be difficult enough, but after factoring in the last few years of inflation and economic rockiness, it's a recipe for disaster. While the current credit card debt for the United States sits at $1.079 trillion (a record high), for those who are more averse to paying interest, the promise of buy now, pay later (BNPL) apps can feel like a welcome relief this holiday season. However, despite the short-term ability to push bills down the road, it turns out BNPL apps could land you in more financial trouble than they're worth.

According to Consumer Reports, more than a quarter of the U.S. consumers surveyed in 2022 had used a BNPL service of some kind to pay for an online purchase. In fact, the Consumer Financial Protection Bureau found that the five biggest BNPL companies (Affirm, Afterpay, Klarna, PayPal, and Zip) handled a total of $24 billion in purchases in 2021. So it's safe to say, if you haven't already seen a buy now, pay later service option, you more than likely will in the near future. And while the interest-free nature of these services is obviously appealing to many people, they can ultimately lead to a slippery debt slope that can wreak havoc on even the most well-intentioned spending budgets.

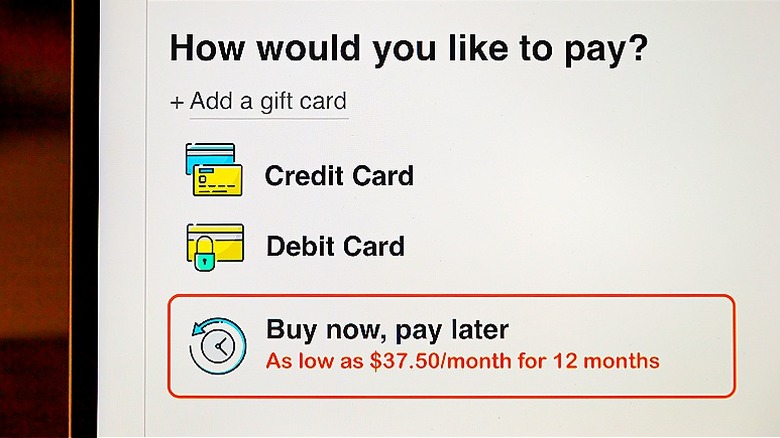

How buy now, pay later apps work

BNPL services allow consumers to utilize short-term financing to cover purchases. After making an upfront payment, shoppers can then pay off the remaining balance over time. Buy now, pay later apps all generally rely on the same "pay in four" schedule, allowing consumers to divide up their purchase total into four smaller installments. Most of these services don't charge interest and are generally easy to qualify for, making them dangerously easy to use. As an added bonus, these loans don't typically affect your credit (as they use soft credit pulls), which can make them even more appealing.

However, buy now, pay later services have important downsides to consider, particularly if you're shopping more than usual, like during the holidays. For one, since many services force users into autopay, you can run the risk of overdraft fees if the payment hits your bank account when you aren't expecting it. While all buy now, pay later services specify the dates of payments upfront, it can be easy to forget the exact dates you agreed to.

It's also worth noting that your payments can still continue even if you have to return the item you financed, which often happens after the holidays. So make sure to keep track of the store's return policy and keep all tracking information for returns. Also, due to the popularity of these payment services, many providers are also offering longer-term loans. These loans can be confusing, as well as misleading for consumers. Plus, according to Consumer Reports, many can carry interest rates as high as 36.99%, which is higher than the average credit card interest rate (currently at 20.72%), in addition to late fees upward of $30.

The financial consequences of BNPL use

In Consumer Reports' aforementioned survey, the nonprofit found that a lot of people are using BNPL services in financially dangerous ways. For instance, 24% of users made BNPL payments using a credit card. To make matters worse, CR found that 10% of users reported having four or more concurrent BNPL purchases at a time (a scenario that can easily happen with holiday shopping, too). Not only are these choices a recipe for missed payments and failed budgets, but the long-term credit ramifications of these decisions can have serious implications on many facets of your life.

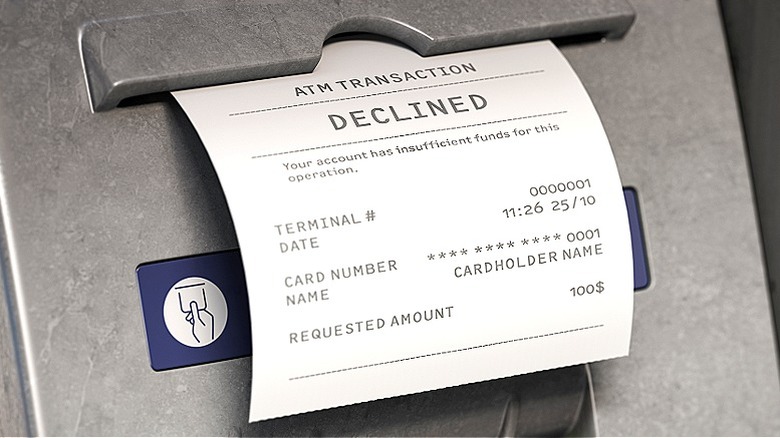

Missed and late payments combined with high credit utilization ratios and excessive debt can all negatively impact your credit report (and, consequently, your credit score). Bad credit can make it extremely difficult to qualify for loans, get affordable insurance, rent an apartment, sign up for utilities, find a cell phone provider, or even get another credit card. The ability to put off debt through BNPL services can lead to a fast accrual of debt with no way out, and the risks associated with the services are becoming more obvious with every year.

For example, the Consumer Financial Protection Bureau found that consumers are increasingly facing late fees, with 10.5% of borrowers charged at least one late fee in 2021 compared to 7.8% in 2020, while a 2023 survey from The Motley Fool Ascent found that 26% of respondents reported having had a late or missed payment. If using a BNPL service on an item is ultimately costing you more money, it might be best to skip the service altogether and find another way to purchase your gifts this holiday season.