Why You Should Think Twice Before Aggressively Paying Off Student Loans

In October 2023, student loan repayments for federal student loans began anew. After a lengthy pause in mandatory repayments on student loans that came about during the COVID-19 pandemic, the federal government once again resumed business as usual regarding student loan debt. The total bill was $1.74 trillion as of September 2023, with about 43 million Americans counting themselves among the collegiate debtors. Those aged 35 to 49 collectively owe the most in student loans with $624.4 billion in debt and the second-highest average per borrower, standing at $42,767.

Individuals who have recently left college or have been diligently making payments — the pause notwithstanding — for a decade or longer may view this change as something of a spark. Doubling down on loan repayment to become debt-free seems like a positive solution to this otherwise long- term and costly problem. But, a number of factors make aggressive student loan repayments a bad financial idea. Of course, everyone's individual circumstances will be their own, but for the vast majority of student borrowers, this repayment strategy's obverse is actually the best route forward. As contradictory as it may seem, getting aggressive about not paying off student debt is likely to serve you as the best course of action.

Student loans have low-interest rates

First and foremost, student loan debt is some of the cheapest you'll incur throughout your lifetime. Mortgage loans are generally the cheapest lending product you will find, but student loans make their way up near the top of the pack and can even surpass mortgages on occasion. The average existing borrower sees an interest rate of 6.87%, with federal interest rates set at 5.5% for all new borrowers in the present.

As a simple matter of principle, student loan debt is cheaper to manage than any lending product you'll encounter in this present moment, mortgage rates included (considering a national average on 30-year fixed rates of 7.27% as of March 4, 2024). Therefore, student loans, which many would categorize as "good debt," should be placed at the back of the pack when it comes to repayment priority.

Indeed, even if you're free of credit card debts and/or other high-interest repayment obligations, you're likely to see a higher rate of return on retirement and your other investment accounts than the negative figure that guides your student loan interest. This means you'll make more with every dollar you invest than you would save by placing it against your student debt. The opportunity cost found when balancing saving versus debt payoff strategies dictates a smarter course of action than one prioritizing student loans simply because they're a part of your debt burden.

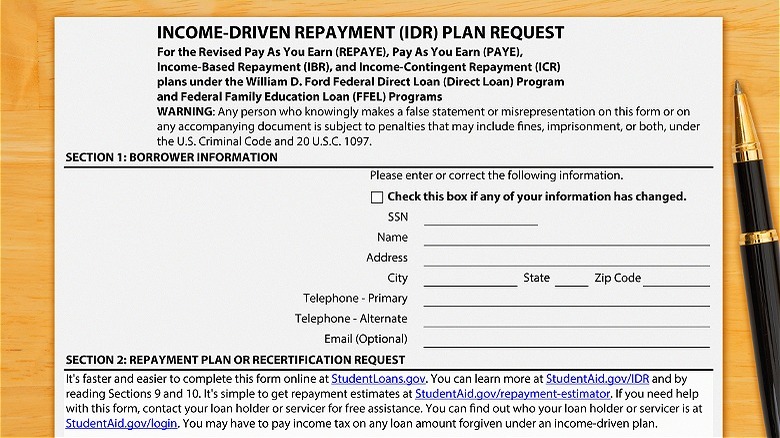

How income-driven repayment plans work

Regardless of your loan's interest rate and any calculations that might come as a result, the landscape surrounding federal student loan repayments is more complicated than any other lending product you may be servicing. The federal government has developed a series of income-driven repayment plans, chief among them the SAVE and PAYE plans, that reduce your monthly repayment burden by using your income as a guide for the figure rather than the total balance owed. Most importantly, at the end of 20 or 25 years of repayments, the remaining balance will be forgiven.

What this means for federal student loan borrowers is that paying the least amount of money possible over this repayment duration will result in a clean slate, while keeping as much money in your pocket as possible. Many borrowers will be eligible for $0 monthly payments as a result of increased income exemptions (225% of the poverty line for the SAVE plan) and a maximum threshold of 5% or 10% of your discretionary income depending on the plan (SAVE and PAYE, respectively).

For millions of borrowers in America, enrolling in one of these income-driven repayment plans will translate into total forgiveness of whatever is left of their student loans from the moment they make the switch. This monetary swing in your favor can truly transform the rest of your financial life and it's absolutely crucial you look into eligibility for yourself.

The possibility of future debt forgiveness

On a broader scale than even these IDR repayment plans, the Biden administration entered office with a promise to make drastic changes to the way student loans are managed and repaid. Included in these campaign priorities was a commitment to forgiving a large volume of student loan debt. While the Supreme Court may have scuttled the White House's plans for the time being, public and political will still holds these goals in high regard.

Regardless of the repayment plan you choose for your federal student loan, there remains a viable path toward blanket loan forgiveness for millions of U.S. borrowers at some point in the future. The public's desire to see this issue resolved hasn't been abated and so pressure from 43 million American borrowers is likely to keep this goal among the forefront of political talking points until a resolution is reached. It may very well be that even if you've applied for an income-driven repayment plan that promises to forgive your debt two decades from now, those student loans may be discharged earlier by forthcoming congressional or administrative action.

The long and short of it is that there are plenty of reasons to push student loan repayments down toward the bottom of your priority list and not aggressively pay it off. Whether your loans are likely to be forgiven or not at some point, U.S. educational debt remains a hot-button issue with plenty of political activity behind it and a relatively cheap personal price tag when compared to the cost of maintaining other types of debt.