11 Reasons Why U.S. Retirees Might Regret Moving To Spain

We may receive a commission on purchases made from links.

Spain is an enchanting destination, offering visitors an attractive blend of teeming metropolises, charming villages, stunning vistas, and captivating coastlines. With these highlights, it's no wonder this Iberian nation is the third most visited country in Europe, falling only behind France and the U.K. Underneath the conspicuous holiday pull, Spain makes a compelling case for a longer-term stay. Seniors looking for the best places to retire outside of the United States often land in Spain, due to its slower pace of life, vivacious street life, diverse landscapes, high standard of living, and convenient location in Western Europe. The numbers are clear.

Over a recent 10-year period, the number of U.S. citizens retiring in Spain soared more than 50%. According to data published by Spain's National Statistics Institute, the tally of Americans calling Spain home in their golden years jumped from 27,856 in 2012 to 41,953 in 2022. Although these elderly expats are spread throughout the country, they tend to concentrate in populated hubs, such as Madrid, Barcelona, Malaga, Valencia, and Alicante.

Spain offers a retirement-specific non-lucrative residence visa, making it easy for seniors to live in the country for extended periods. A 2025 Harris Poll revealed that 52% of U.S. adults believed a higher standard of living could be achieved abroad, while another 43% thought the international move would make them happier. Despite these numbers, some U.S. transplants realize Spain might not deliver the picturesque golden years they had envisioned. Many Americans actually end up picking up and moving to another European country or heading back home altogether. To avoid the hassle and costs, understanding the main reasons U.S. retirees might regret moving abroad can help you make an informed decision.

1. Weak exchange rate

The persistently poor exchange rate between the U.S. dollar and the euro is one of the largest and unforeseen financial burdens to retiring in Spain. This relative weakness of the dollar puts Americans at a severe disadvantage, affecting every single purchase and investment denominated in the shared European currency. As of January 2026, the European Central Bank pegs $1.00 at €0.86. Put another way, €1.00 is equal to $1.16. Thus, retirees spending dollars in Spain lose about 14% of purchasing value on every single purchase. Imagine losing 14% of your nest egg overnight simply for retiring in a place with a more valuable currency.

Consider that the median retirement savings peak between the ages of 65 and 74 at $200,000, according to Kiplinger. For perspective, the sheer act of moving to Spain renders that sizable nest egg to $172,000 in real spending power. Beyond daily expenses, such as groceries and fuel, and large purchases, such as real estate and cars, this exchange rate also diminishes retirement income in the form of Social Security benefits and retirement fund withdrawals. Unfortunately, the dollar fluctuation against the euro has been the norm for the past 20 years, and experts don't see the greenback overtaking the European bloc's currency any time soon.

2. Unforeseen expat fees

Moving to Spain can dredge up some hidden expat costs that seniors don't think about beforehand. These unforeseen expenses are usually front-loaded in the transition process, closely associated with the processing of visa applications, the establishment of bank accounts, and the broader navigation of a foreign country's financial, bureaucratic, and legal systems. Of course, these expat relocation expenses vary greatly between retirees, often determined by their retirement savings, visa eligibility, and overall familiarity with the intricacies of the Spanish system. Covering some of the general costs can give seniors an idea of what to expect.

On the financial front, expats often experience higher-than-anticipated costs when they first move to Spain due to unexpected foreign spending fees. Most notably, expats are often burdened with foreign transaction fees and currency conversion fees when first moving to Spain. These are avoided long-term by obtaining a European bank account and accompanying credit or debit card. Before these are established, some U.S. banks may be hitting expats with these penalties on every purchase. Depending on your credit score, you'll be relieved or frustrated to know it has no bearing in Europe.

Another source of oft-overlooked transition fees is the visa process itself. Professional assistance in obtaining the long-term visas most commonly sought by retirees can cost about €350, according to the Expat Agency. Renewing the visa hovers between €300 and €450. Hourly legal help is around €55 per hour, while an in-person translator runs roughly €40 per hour. Taxes for Expats estimates that these costs can cost anywhere from $5,000 to $15,000, with longer-stay visas costing more of a financial investment.

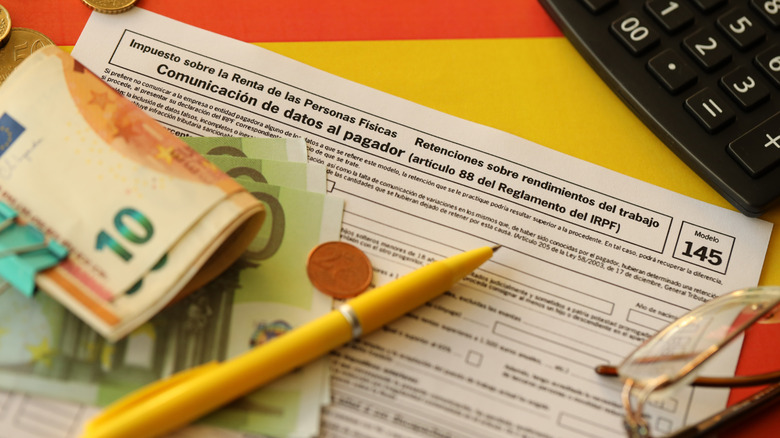

3. Elevated and progressive income taxes

One of the most potentially expensive myths about taxes people need to stop believing is that Uncle Sam doesn't take his cut from U.S. expats. The U.S. and Eritrea — a small Northeastern African nation — hold the unenviable title as the only countries to tax their citizens regardless of their physical location, according to the Tax Foundation. What's the big deal about continuing to pay taxes when retiring in Spain, you might wonder? Well, you'll be owing taxes in your newfound home, too. U.S. citizens who retire in Spain face the potential of overlapping taxation on specific types of income. Spain designates a person as a taxable resident if they spend over 183 days in the country or if Spain is judged to be their primary center of economic activity. The latter definition is more ambiguous and may require some professional consultation to determine if it's triggered.

The national tax rate starts at 19% for income up to €12,450, but it can reach 47% for income exceeding €300,000. The U.S. has a progressive tax structure, too, but it tops out at 37%. That means high-earning retirees face potentially 10% higher taxes. Keep in mind that this doesn't only pertain to the percentage of people returning to work after retirement. In addition to earned income, Spain also taxes various forms of retirement income, including pensions and withdrawals from 401(k)s and individual retirement accounts. Social Security disbursements are a welcome exception to this rule, for which the U.S. and Spain have an agreement to prevent double-dipping on this crucial retirement support.

4. Risk of double taxation

Whether you're managing a fixed income or you've earned enough to retire rich, handling a tax burden from two different countries is a serious financial balancing act. Unless you're working through retirement, you'll be largely spared from taxes on earned income, but Spain still levies hefty savings taxes. This taxation can be triggered by income-generating investments common in retirement portfolios, such as dividends, interest yields, and even capital gains from certain assets. You could find yourself suffering double taxation on the primary funds you planned to use throughout retirement, making your golden years abroad much tighter than initially anticipated.

Similar to general income tax, savings income is taxed on a progressive scale. Many seniors regret moving to Spain upon realizing these overlooked financial burdens. The initial €6,000 earned is taxed at 19%. This goes up to 21% for any eligible income between €6,000 and €50,000. Taxable income between €50,000 and €200,000 gets hit with a 23% tax. If you're pulling in over €200,000, you can expect a bill of 27%. These savings income taxes top out at 30% for anything over €300,000. The U.S. and Spain have entered into a long-standing double taxation treaty, seeking to clarify which country has a claim to certain income and to protect citizens. However, the complete avoidance of dual tax burdens isn't guaranteed, and taxpayers must do the legwork to determine their eligibility and secure the protections.

5. No earnings permitted through a long-term visa

In addition to a progressive tax structure above U.S. rates and the possibility of overlapping tax liabilities, retirees who plan on working while retiring in Spain run up against strict visa limitations. There's no retirement-specific visa for the country, yet most people aim for the non-lucrative visa when spending their golden years in Spain. This is the go-to visa for those looking to retire because it permits non-citizens of the European Union to stay long-term in the country. Of course, retirees need to meet certain eligibility requirements. Among these are proof of savings 400% above the country's Public Multiple Effects Income Indicator, according to the Government of Spain.

My Spain Visa reports that these proofs of funds come out to about $31,050 annually or $2,588 monthly. That may seem reasonable, especially compared to the average cost of living in the U.S., but this non-lucrative visa, as the name suggests, precludes you from working in Spain, either for a local, international, or U.S.-based company. The government wants to see these funds as passive rather than active income, meaning retirees need to have a decent amount of savings to even qualify for this visa. To be sure, other visas allow U.S. citizens to work while in the country, but they're often provided for short periods.

6. Expensive real estate

Retirees often pursue retirement in Spain with the presumption that everything will be cheaper than in the U.S. Although the overall cost of living in many European countries is indeed lower, this affordability isn't evenly spread across different expenses. For example, the average home in Spain is quite costlier than stateside. It's tough to compensate for this higher expense through other budgetary items, since housing comprises such a larger percentage of the average retiree's net worth. Wealth Tender suggests that home equity accounts for at least half and, in some cases, nearly two-thirds of the median net worth in the U.S. Generally, the older the person, the more their nest egg is tied up in housing.

Statista places the average home price in Spain at €3,151 per square meter. Using the ECB conversion rate, which equates one euro to $1.16, that translates to roughly $340 per square foot. In contrast, the average housing price in the U.S. is $220 per square foot, per the Federal Reserve Bank of St. Louis. According to Spain-based legal firm Lawants, the real price of homes tends to exceed the list price by 10% to 15% once retirees factor in related taxes and professional expenses. If you end up keeping your property in the U.S., you can always turn that second home into an asset.

7. Extreme regional cost fluctuations

Spain is reputed as a low-cost country that's appealing to Americans, but this vague description risks painting the country with a broad brush. In reality, this country of around 49 million people is larger than California, stretching nearly 200,000 square miles across the Iberian Peninsula. This expansiveness contributes to extreme regional variability. For retirees looking for an affordable place to retire outside of the U.S., this economic diversity should be of utmost concern. You're simply not going to experience the same living standards or routine expenses in an extremely sought-after or well-populated area, such as Barcelona or Madrid, as you would in the lesser-known regions. A helpful analog for the U.S. would be comparing the cost of living between New York City and Los Angeles with that of Omaha and Fargo. The difference is undeniable.

Let's focus on housing expenses again, since mortgages and rents tend to outweigh other costs. Statista suggests that the average home in the Community of Madrid, home to the country's capital, is $527 per square foot. This elevated rate is only beaten out by Catalonia, whose regional capital is Barcelona, where home prices average $543 per square foot. For comparison, the countryside and less-visited regions of Murcia and Extremadura offer the most affordable homes in the country at $167 and $150 per square foot, respectively.

8. High value-added tax (VAT)

In addition to a higher top-tier tax rate, Spain implements a hefty value-added tax (VAT). This concealed tax is financially irksome enough to make some retirees regret moving to Spain. The European Union sets a blanket, minimum 15% VAT, and it's up to individual countries whether they want to add more. For its part, Spain places a standard VAT of 21%. That means many services and goods you purchase within the country are subject to an additional 21% surcharge. There are exemptions for routine and essential purchases, yet these items are only slapped with a lower rate, not offered tax-free. For instance, restaurants, accommodation, and public transportation only see a 10% VAT. Furthermore, books, grocery goods, and essential healthcare products have a 4% VAT.

On the other hand, the U.S. doesn't apply a VAT on any goods or services. Instead, state and local governments rely on sales taxes to achieve the same funding as this European-focused mechanism. Still, Europe's flat VAT of 15% exceeds many of the states with the highest sales taxes. While relatively low compared to some of the upfront costs associated with retiring to Spain, seniors should think about how these add-on costs accumulate over time, eating away at their nest eggs.

9. No Medicare coverage

The U.S. Census Bureau highlights how the percentage of seniors who have private and public health insurance is dwindling. Between 2017 and 2022, the number of U.S. adults 65 and older with dual coverage fell from 47.9% to 39.6%. This means that more seniors are becoming solely dependent upon Medicare for their health coverage in their golden years. Although all elderly couples should think about their medical coverage, those heading outside of the country are automatically at greater risk. Unfortunately, Medicare doesn't offer health insurance coverage for retirees living in Spain, leaving seniors open to potentially expensive healthcare costs.

Expatica estimates that private health insurance coverage in Spain can cost up to $290 per month. That's roughly $3,480 annually. Again, that might not seem too bad compared to U.S. health insurance costs, but it's an often unexpected cost for Americans retiring in Spain. These healthcare expenses only become more onerous as an individual's needs rise. Long-term care isn't much cheaper than in the U.S. For example, retirement homes average anywhere between $1,160 and $4,060 per month, or $13,920 and $48,720 per year, according to Ciudad Patricia.

Spain indeed has an excellent public healthcare system, but the non-lucrative visa that most retirees in Spain pursue doesn't guarantee access to it. Even if you live in Spain for a decade straight, you're not guaranteed entry, making these private healthcare costs a crucial part of your budgeting for potential retirement in Spain.

10. Moving and travel expenses

Many retirees dive into retirement with a short-term focus on capitalizing on the newfound time, freedom, and financial independence. Through this hyper-focused lens, moving to Spain feels like a once-in-a-lifetime adventure rather than a consequential decision. Some of the financial ramifications that can make U.S. retirees regret moving to Spain are the unexpected costs of moving and traveling. Spain is thousands of miles from the U.S. and across the Atlantic Ocean, meaning the process of relocating to the country and every trip back home requires an international flight.

The cost of physically moving your life from the U.S. to Spain can cost anywhere between $3,500 and $10,000, according to Sirelo. Generally speaking, these costs rise based on the amount of stuff you're moving and the distance from your current home in the U.S. to your new place in Spain. For instance, a one-bedroom apartment may be half the cost of a three-bedroom home. On top of the initial move, retirees need to consider the long-term cost of flying back and forth to visit friends and family. Booking suggests that the average round-trip flight between the two countries can cost upwards of $1,269 per person. For a retired couple, a single visit home could reach over $2,500 on flights alone.

11. Expensive fuel

Europe is often celebrated for its well-connected and efficient public transportation system, and Spain is no exception to the rule. In fact, it's home to Europe's longest high-speed railroad system, spanning over 4,000 kilometers, or about 2,500 miles. China is the only country to outperform Spain in this achievement. Still, retirees who want to have a vehicle in Spain may find the unexpectedly elevated costs unnecessarily burdensome, compared to U.S. standards.

Among the most egregious transportation-related costs is the price of fuel in Europe. AAA estimates that the average price of a gallon of standard gas in the U.S. is $2.83. In contrast, a gallon of gas in Spain will set you back $6.32 per gallon, according to Global Petrol Prices. That means retirees are paying more than twice as much just to get around in Spain compared to America. It's worth noting that Europe measures its fuel prices in liters instead of gallons. Thus, fuel prices can look reasonable at first glance until you see the final bill. There are roughly 3.79 liters per gallon, so you'll have to multiply Spanish fuel prices by this amount to get a per-gallon equivalent for quick contrasting. Buying a vehicle in Spain is more affordable than in the U.S. on average, but Spain still has rates for new vehicles above the European norm, according to Statista.