11 Reasons Retirees Regret Moving To Florida

Florida is often viewed as the crown jewel of the United States' many appealing retirement destinations. Over the decades, millions upon millions of retirees have made their way to the southeastern tip of the country to bask in the warm weather, dip their toes in the ocean, and enjoy the Sunshine State's year-round brightness. Florida's popularity among seniors has actually altered its age demographics, with around 21% of the population comprised of retirees, according to USA Facts.

Unfortunately, Florida's extreme popularity as a retirement hub is starting to work against its appeal as the number of pensioners skyrockets. With pleasant winter weather, hundreds of miles of beachfront property, and various retirement-oriented accommodations, what's not to love about the Sunshine State, you might ask? Well, many retirees have regretted moving to Florida over the years, pointing to various changes in the state's quality of life, affordability, and even weather extremes. Before you make one of the largest financial decisions of your golden years, it's important to consider the downsides of moving to the Sunshine State.

Poor healthcare

Healthcare is the one major expense you shouldn't forget when budgeting for retirement. It's often the single biggest budget item for seniors as health complications begin piling up in their later years. With over 1 in 4 Floridians 65 years or older, you might expect the healthcare system to be among the best in the country. Unfortunately, the Sunshine State doesn't shine bright in this category. Florida's healthcare system consistently ranks low compared to other states in several crucial areas, including successful outcomes, accessibility, and affordability. A 2025 Wallet Hub study ranked Florida at No. 42 in the entire country — among the bottom 10 worst healthcare systems.

Long-term care in Florida, which Medicare tends not to cover, can reach anywhere from $63,000 to over $130,000 per year, depending on how much attention is required, according to 2024 data from Genworth. On top of that, a Zinda Law Group analysis of Centers for Medicare & Medicaid Services data, per Naples Daily News, found that emergency room wait times in Florida can easily balloon to almost three hours. This can spike the costs associated with delayed treatment and increase the risk of negative outcomes from serious issues.

Unfortunately, Florida's healthcare system isn't expected to improve. In fact, many experts see the situation worsening. Some of the biggest hurdles to better care for seniors include a massive shortfall of qualified workers, the rising costs of medicine, and upcoming Medicare cuts, most closely associated with the One Big Beautiful Bill Act

Costly swimming pools

The cost of a swimming pool may seem like an insignificant reason to regret moving to Florida, especially compared to healthcare unaffordability, but the financial burden of these common home features is often overlooked. According to PoolResearch data, there are about 1.59 million pools in Florida — which is roughly 15% of all homes in the state. This means there is a decent chance that any property you might look at will have a pool. While you are likely to understand the appeal after experiencing your first 100 degree Fahrenheit day in the Sunshine State, your first maintenance bill might make you sweat even more.

Owning a pool is a financially consuming endeavor. Estimates suggest that cleaning a pool can cost anywhere from $80 and $150 weekly. That translates to $960 per year on the low end and $1,800 on the high end — a serious expense for those living on a fixed income. For those hoping to install their own pool in Florida, it's important to realize just how expensive they are. The average in-ground pool in Florida can cost anywhere from $35,000 and $65,000 — although customization can easily skyrocket costs for $200,000, per VanKirk & Sons. While the idea of chilling poolside in your backyard on a sunny day in Florida could be an ideal retirement backdrop, the associated costs make many retirees regret the decision.

High skin cancer rates

The Sunshine State lives up to its nickname with anywhere from 221 to 266 days of sunshine per year, depending on where in the state you live, per Current Results. Yet, Florida's unrelenting sunniness isn't without its drawbacks. Tragically, the state also has one of the highest incidence rates of skin cancer in the country, owing in part to year-round exposure to harmful sun rays. Every year, 8,000 Floridians receive the gut-wrenching news, and incidence rates are only increasing.

Even though skin cancer has one of the highest survival rates, and early detection can further improve those odds, treatment isn't cheap in Florida. Sidecar Health estimates that a single visit to a dermatologist can cost as much as $133 in the Sunshine State, not including any additional tests or imaging. These costs only increase if complications are found. Surgeries for skin cancer can range from $5,000 to $10,000 for those without insurance. This is why diligent sunscreen application can be especially important. However, it's worth noting that quality sunscreen can be expensive due to the premium-grade ingredients included to help protect skin from damaging ultraviolet rays.

Skyrocketing HOA fees

Florida's real estate market isn't only plagued by rising home prices. Retirees also face steep homeowner's association (HOA) fees. Many apartment complexes, neighborhoods, and even retirement communities in the Sunshine State charge these monthly fees to residents to cover the costs of general maintenance of shared areas, such as pools, gardens, sidewalks, and roads. While these dues are common across the U.S., they're uniquely prevalent and expensive in Florida. The state is home to around 50,100 HOAs, the second most in the country, only behind California, according to iPropertyManagement.

These groups are so prevalent that 64% of property owners are subject to an association. But it's not just homeowners. Renting property in the state can also place you in an HOA. In fact, 40% of the general population of Florida lives in an area with these groups. iPropertyManagement notes the median HOA fee in Florida is a wallet-pinching $230 monthly, which works out to be $2,760 annually. That's a serious bite of your retirement savings, especially if you're only in Florida for part of the year. The increase in HOA fees affects homebuyers, especially seniors, by cutting into already tight housing budgets.

Rising insurance premiums

In the past three years alone, home insurance premiums in central Florida have grown by 40%, according to Central Florida Public Media. As of October 2025, the average home insurance premium in Florida is around $8,800 annually, per MoneyGeek, although some providers can and do charge upwards of $12,000 to $15,000. These figures are much higher than the national average, which places additional financial pressure on retirees. Unfortunately, experts anticipate home insurance premiums to continue rising as the underlying causes, like climate change, remain unchanged.

Several sneaky factors raise property insurance rates, but the Florida government's intervention into the insurance system plays a unique role. The Citizens Property Insurance Company is a state-sponsored mega-insurer designed to provide a bulwark against an industry-wide wipeout as insurance providers leave, or threaten to leave, over increased risks associated with covering Floridians. However, it faces high liability as the largest carrier of policies in the state. As a result, recent state legislation has made it harder for residents to sue private insurance providers — for things like insufficient coverage or payouts — in order to try and court favor with private insurance providers in the hopes they will stay in the state and help mitigate the pressure on the state system. Unfortunately, this does nothing to help lower insurance rates for Floridians.

Prevalence of natural disasters

Florida is no stranger to natural disasters, with hurricanes, flooding, and torrential rain hitting the peninsula regularly. The state's coastal positioning between the Gulf of Mexico and the Atlantic Ocean, along with its long, thin shape, makes it uniquely susceptible to adverse weather. In fact, the National Centers for Environmental Information report that the state was hit with 94 disaster events between 1980 and 2024. That bone-chilling stat includes floods, wildfires, winter storms, freezings, droughts, severe storms, and hurricanes or cyclones. Put another way, the Sunshine State receives around two natural disasters annually, placing retirees and their property at significant risk.

During that 24 year period, it's estimated that the 36 hurricanes/cyclones that hit the state cost a total of between $300 and $420 billion, not including any of the other natural disaster events. Even worse, between 2020-2024 alone, the state experienced 34 separate billion-dollar disasters. These unforeseen expenses can place significant stress, not to mention costs, on seniors in Florida.

Booming real estate market

Despite the prevalence of natural disasters, Florida's real estate market has exploded in recent years. Since 2020, the population has grown by a staggering 8.2%, per the U.S. Census Bureau. This rapid population surge has placed immense pressure on Florida's real estate market, leading to a significant housing shortage.

As a result, housing prices have risen dramatically. Retirees who purchased property decades ago have seen their wealth spike, while many of those considering a move to Florida are now outpriced. As of October 2025, Zillow places the average home in the state at around $377,000, which is slightly above Zillow's U.S. average home value of $363,932. Although home prices are soaring around the country, Florida's real estate values have outpaced the national average, according to Cotality. In Miami, in particular, home prices have eclipsed the state's average by 60%. Retirees could find themselves facing exorbitant housing costs, a potentially major hurdle to spending their golden years in the Sunshine State.

Misleading tax laws

Florida is one of the nine states in the country that does not levy an income tax on its residents, allowing retirees to keep more of their income. Plus, while other states tax Social Security benefits, pensions, and other forms of retirement income, Florida seniors don't have to give up any portion of their anticipated nest egg. However, many retirees don't take into account other forms of taxes. Instead of merely forgoing taxes altogether, the state finds other ways to compensate for its lack of income tax — usually in the form of higher property and sales taxes.

Over the past five years, property taxes in Florida have surged by a whopping 60%, Kiplinger points out, rising along with a spike in home prices. This has placed tremendous stress on retirees while also discouraging newcomers from putting down roots in the state. Experts trace climbing property taxes to the state's recent population boom, especially in densely populated cities such as Miami, Tampa, and Jacksonville. Seniors need to consider whether unusually high and rapidly rising property taxes are worth investing in property. Plus, don't forget about state income tax — Florida tacks on a standard 6% on most purchases, whether it's a product or service. While that is already one of the highest in the country, some local areas in the state charge as much as 8%.

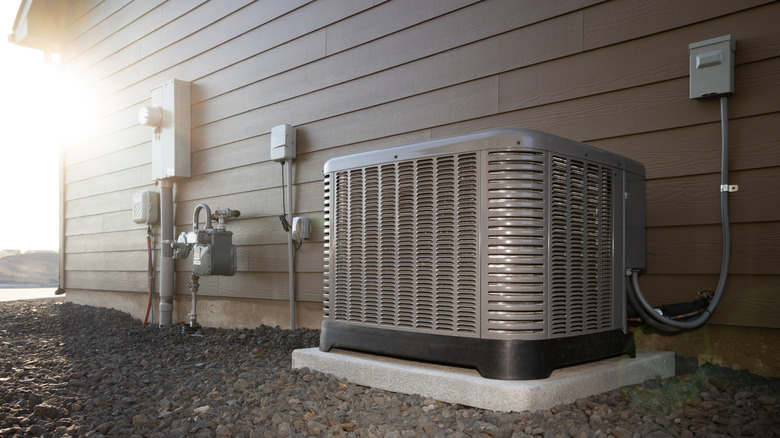

Excessive heat

Anyone who has stepped foot on a Florida beach in the summer can attest to how it can get. Beyond merely making it uncomfortable to be outside, seniors also must face the larger financial impact of this extreme heat. In contrast to other areas of the country where air conditioning is only required a few months out of the year, it's not uncommon for Floridians to blast their ACs for more than half of the year, especially in Southern Florida. While you're focused on optimizing comfort in the moment, the utility bill at the end of the month may make you squirm.

Costs to run your air conditions can range between $120 and $200 monthly, depending on the size of the house. That means retirees are looking at an annual bill of $1,440 and $2,400 just for cooler air. These figures also don't take into account routine maintenance, repairs, and replacements — all of which are more common the more frequently a unit is used. In warmer areas, like Florida, the lifespan of an HVAC unit can be slashed down to just 10 to 15 years. However, extreme temperature fluctuations can further erode this timeline.

Demanding building codes

For many retirees, building a home is a critical part of completing a move to Florida. Even if you're looking to buy a preexisting home, many of Florida's real estate properties were built in the 1960s and 1970s, meaning plenty of updates could be required. In some areas, nearly one-third of the houses were constructed in this era. Unfortunately, Florida tends to have higher construction costs, making it more expensive for retirees to build their own home or make improvements to an existing one. Experts place the blame for higher-than-average construction expenses on statewide labor gaps, growing permitting complications, rising material costs, and booming demand. One of the sneakiest reasons that building and/or fixing up a home is so pricey in Florida is the state's stringent building codes.

Before the 1990s, Florida took a laissez-faire approach to construction — with no uniform statewide policy. Instead, it was a patchwork of localized rules, although many areas remained hands-off. The state's relaxed method only finally came under scrutiny following Hurricane Andrew in 1992. This prompted the creation of state-enforced building codes. However, additional natural disasters have only made those requirements more demanding and restrictive — making it more expensive for builders to adhere to them. Whether building or renovating, retirees can expect exorbitant price hikes associated with these more exacting codes.

Limited public transportation

Florida is widely criticized among locals for its lack of public transportation. This is due, in part, to the state's massive population of 23 million – the third-largest in the country — and the state's sprawling size. While Florida has its fair share of buses, trains, and other forms of public transit, the system sizes aren't always in line with the number of Floridians in an area. For instance, Tampa's public transportation system often ranks among the worst in usage and coverage when compared to other significant metro areas. A 2017 Tampa Bay Times report found that the city spends tens of millions of dollars less on public transportation than cities of comparable size, and, as of 2025, the problem has not significantly improved.

Although there are plenty of car brands retirees will instantly regret buying, overpaying for a lack of public transportation is another headache you might want to avoid in your golden years. Florida's deficient transit systems leave retirees paying for costly maintenance, rising fuel costs, and expensive vehicles. Plus, there's always the looming specter of not being able to drive at some point in your older years, making a functioning public transportation system that much more important.